New Zealand’s liquid market highlights depth of dry powder

23 Mar 2021

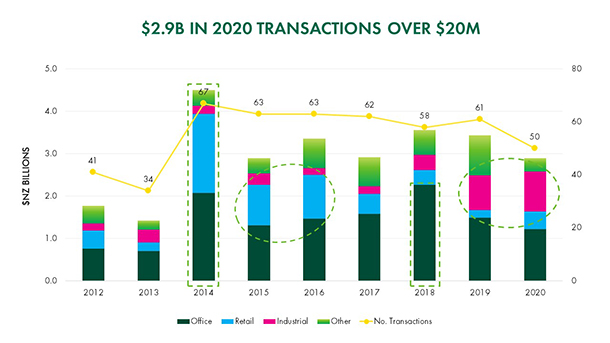

After the first 2020 lockdown was behind us, H2 saw the continuation of a strong investment market in New Zealand, although there was still a cautious but optimistic air to most campaigns. Ultimately, we saw continued asset price growth across the main markets and total transaction volumes of $2.9 billion, in the $20 million plus space for the year.

The circa $3 billion in property trades is consistent with the past six years volumes albeit the asset mix has changed significantly from a heavy retail and office weighting in the mid-2010s, to a strong industrial and office skew in 2019 and 2020.

During our latest CBRE Market Outlook: Restart the Uneven Recovery, I highlighted that up until 2014 the New Zealand market had suffered from a lack of participation from international investors due to liquidity question marks. However, in 2014 a couple of new international entrants, namely PSP from Canada and GIC from Singapore, placed $2 billion plus of capital in New Zealand office and retail, effectively rubber stamping our market and cementing a new level of appetite.

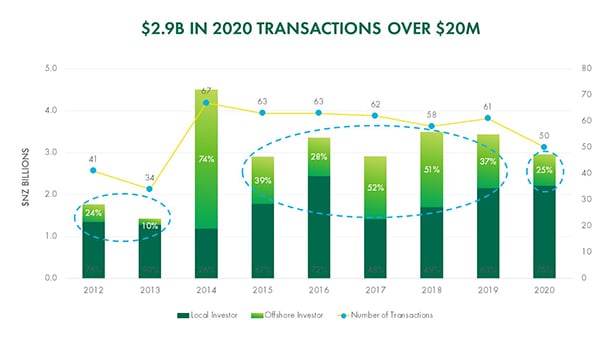

In 2020, the market reverted slightly back to historic local vs off-shore investor activity, largely influenced by the border closures but particular categories of off-shore investors still remained active and interested, keenly awaiting the borders to open again.

In 2020, of the deals that CBRE transacted, 36% of bids were from off-shore buyers, however these groups only concluded 25% of the completed deals, mostly we believe due to an inability to demonstrate acquisition conviction from afar combined with travel restrictions. This notwithstanding, we still experienced consistent total transaction volumes, even in a year where 6 to 8 weeks was in strict lock down. 2020 was a depth test for the local market and we quickly proved that we have more than enough appetite locally to sustain historic volumes and even firm prices at the same time.

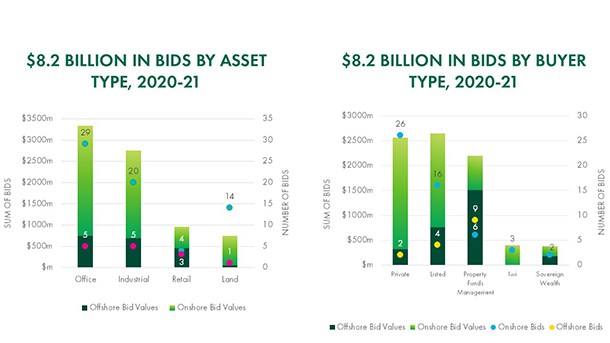

Specifically, 2020 saw the New Zealand-based private investors as well as local listed property entities step in to transaction bidding in a big way, with the only meaningful bid volumes from off-shore coming from the property fund managers, mostly via Singapore and Sydney. In terms of sectoral focus, office and retail took a back seat to the industrial and logistics sector which remains flavour of the month.

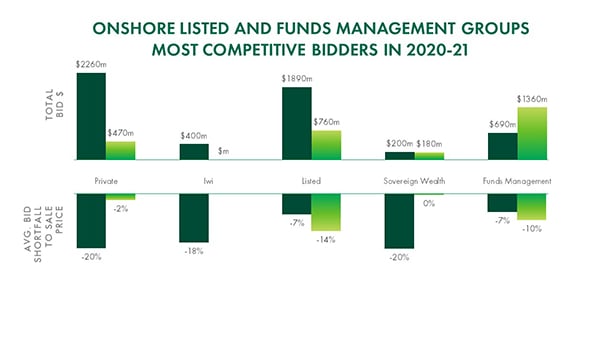

An interesting observation is the extent to which the various buyer groups are missing deals. As in a normal year, a large number of the private buyers remain bargain hunters and on average those private bidders who missed deals, under-shot the purchase price by 20%, closely followed by iwi groups missing by 18%. Local listed groups stepped up in 2020 and were the most active and competitive investor group in the $20 million plus space, finally being in a position to acquire accretively.

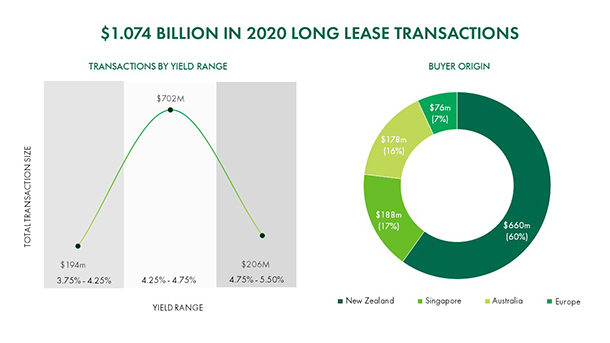

Quite clearly the trajectory of investment yields is now well in to the 4s and may even be threatening the 3s when considering long-lease transactions. We have seen over $1 billion in long-lease deals transacting in 2020, and the sample size seems sufficient enough to prove a very strong and deep capital market appetite.

For the rest of 2021, we expect to see continued depth of bidding and an improving international capital appetite due to the prospects of borders reopening. Although the strength of the occupier market seems to be a consideration, New Zealand overwhelmingly is viewed as an outperformer in the current environment, so there is an expectation that our country will outperform in the global competition for capital.

What does it mean? It seems we have a massively liquid market, which indicates that investor confidence remains high. This is notwithstanding some challenges, but these are small compared to most other investment destinations.

The circa $3 billion in property trades is consistent with the past six years volumes albeit the asset mix has changed significantly from a heavy retail and office weighting in the mid-2010s, to a strong industrial and office skew in 2019 and 2020.

During our latest CBRE Market Outlook: Restart the Uneven Recovery, I highlighted that up until 2014 the New Zealand market had suffered from a lack of participation from international investors due to liquidity question marks. However, in 2014 a couple of new international entrants, namely PSP from Canada and GIC from Singapore, placed $2 billion plus of capital in New Zealand office and retail, effectively rubber stamping our market and cementing a new level of appetite.

In 2020, the market reverted slightly back to historic local vs off-shore investor activity, largely influenced by the border closures but particular categories of off-shore investors still remained active and interested, keenly awaiting the borders to open again.

In 2020, of the deals that CBRE transacted, 36% of bids were from off-shore buyers, however these groups only concluded 25% of the completed deals, mostly we believe due to an inability to demonstrate acquisition conviction from afar combined with travel restrictions. This notwithstanding, we still experienced consistent total transaction volumes, even in a year where 6 to 8 weeks was in strict lock down. 2020 was a depth test for the local market and we quickly proved that we have more than enough appetite locally to sustain historic volumes and even firm prices at the same time.

Specifically, 2020 saw the New Zealand-based private investors as well as local listed property entities step in to transaction bidding in a big way, with the only meaningful bid volumes from off-shore coming from the property fund managers, mostly via Singapore and Sydney. In terms of sectoral focus, office and retail took a back seat to the industrial and logistics sector which remains flavour of the month.

An interesting observation is the extent to which the various buyer groups are missing deals. As in a normal year, a large number of the private buyers remain bargain hunters and on average those private bidders who missed deals, under-shot the purchase price by 20%, closely followed by iwi groups missing by 18%. Local listed groups stepped up in 2020 and were the most active and competitive investor group in the $20 million plus space, finally being in a position to acquire accretively.

Quite clearly the trajectory of investment yields is now well in to the 4s and may even be threatening the 3s when considering long-lease transactions. We have seen over $1 billion in long-lease deals transacting in 2020, and the sample size seems sufficient enough to prove a very strong and deep capital market appetite.

For the rest of 2021, we expect to see continued depth of bidding and an improving international capital appetite due to the prospects of borders reopening. Although the strength of the occupier market seems to be a consideration, New Zealand overwhelmingly is viewed as an outperformer in the current environment, so there is an expectation that our country will outperform in the global competition for capital.

What does it mean? It seems we have a massively liquid market, which indicates that investor confidence remains high. This is notwithstanding some challenges, but these are small compared to most other investment destinations.