Press Release | Intelligent Investment

Lending appetite for New Zealand commercial property is slowly improving…

…but at a higher cost and with more prudent LVR, ICR, and presales.

July 19, 2023

Media Contact

Marketing and Pitch Director, New Zealand

Lending appetite for commercial property investment is showing a small improvement, although Interest Cover Ratio (ICR) and presale requirements are still high, according to a survey report published by CBRE New Zealand.

CBRE’s Q2 New Zealand Lender Sentiment Survey was conducted by CBRE’s Debt & Structured Finance team. It examined the sentiments and intentions of 20 bank and non-bank lenders, which includes pension funds and securities companies, in the second quarter of 2023. Seven international lenders and 13 domestic lenders were included. Of the seven offshore lenders, three were banks and four were non-bank lenders. Of the 13 domestic lenders, three were banks and ten were non-banks.

The survey has revealed that:

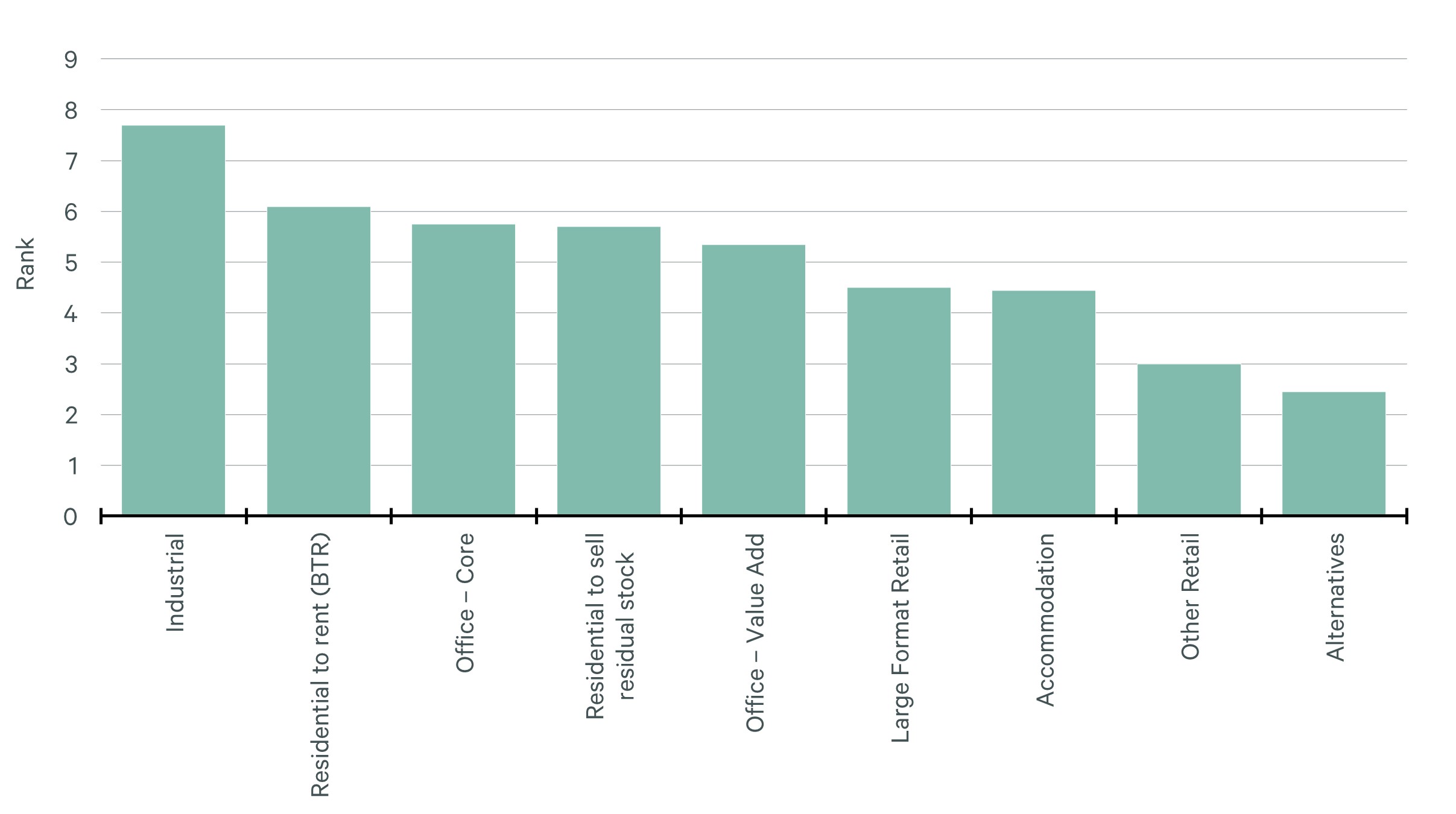

Lending appetite is showing a small improvement compared to last year, mainly for investment property rather than for development loans. Industrial property continues to lead lenders’ sector preference for investment lending, ahead of Build to Rent and core office assets.

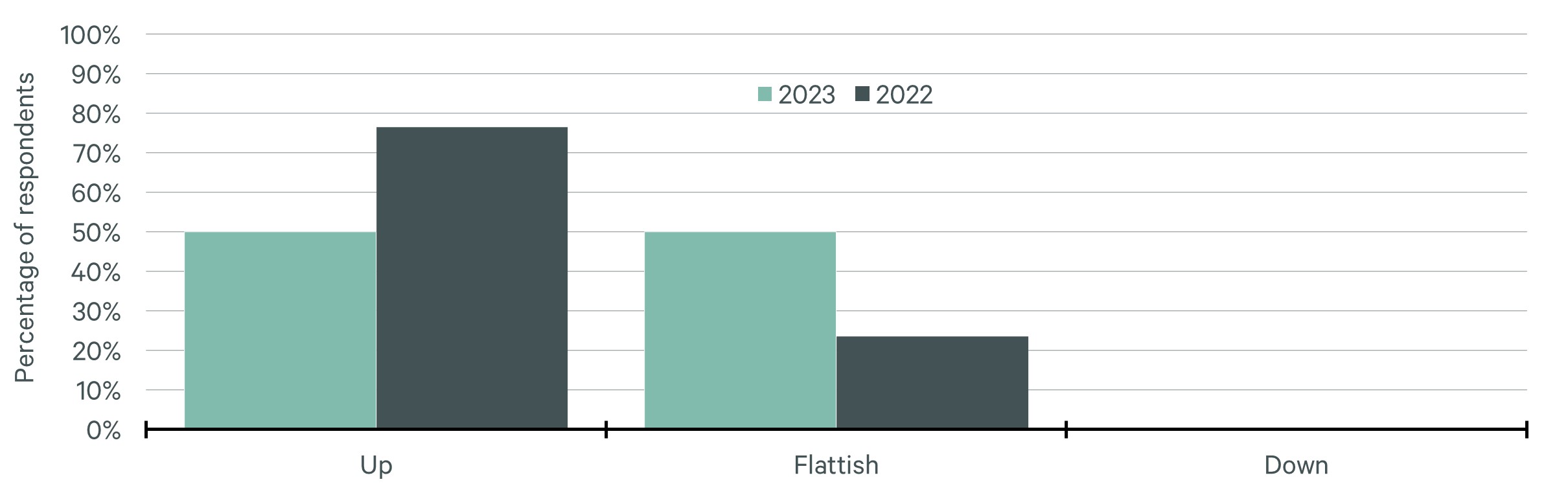

All-in interest rates are likely to continue increasing via lenders’ margins. However, these increases are expected to occur at a slower rate than in 2022 as substantial pricing premiums have already been built in by most lenders through their credit margins.

Loan To Value (LVR) ratios continue to be the bridesmaid to Interest Cover Ratio (ICR) requirements. Bank lenders are seeking a minimum of 1.50x -1.75x ICR cover. For some existing clients they are falling below this level but require a pathway back to 1.50x. Non-banks make up the higher end of LVR capacity, less concerned with LVR and ICR as long as an achievable exit is available, whether via refinance, amortisation, development or divestment.

Figure: Preferred asset class for new non-construction lending (rank from 1 to 9).

Appetite for development lending is towards terrace/townhouse dwelling types. Compared to last year’s survey, there is a significant uplift in required presales – particularly from non-banks – as proof of concept and to help reduce concerns around settlement risk. All lenders are now seeking a current and reasonable level of presales as proof of concept and to help reduce concerns around settlement risk, and banks continue to require presale cover on 100% of debt.

Figure: In the next three months, credit margins on new non-construction loans are likely to move:

Richard Zhao, Director of CBRE Debt & Structured Finance, says: “Credit margins are moderating, therefore pricing increases are slowing, as lenders perceive risks starting to ease. However, although the market is still challenging, our view for borrowers is that the cost of funding is closing in on the peak, and lender appetite seems to be getting better, so if you’re holding on to capital now could be a useful time to examine your options.”

Alex Nikolaou, Director of CBRE Debt & Structured Finance, adds: “It would be advantageous to review capital and debt structures now, with an expert. Options may include refinancing or restructuring. Our advice is ‘don’t sit on your hands’. The bottom line is that we see the challenges that this market presents, and we can add value.”

Zoltan Moricz, Executive Director Research, CBRE New Zealand, says: “In terms of the sectors that are attracting investment lending, industrial property is the most preferred asset class. Also, good core quality office continues to be supported by lenders, with many ranking it as their second or third most preferred choice. And although retail continues to be viewed less favourably by lenders, except large format, in CBRE’s experience buyers remain able to access debt in these market sectors.

“Lender appetite to the residential sector is more polarised. We have seen Build To Rent come up the order since our last survey. Residential to sell for residual stock (dwellings remaining unsold upon physical completion of a new development) is ranked as most preferred asset by seven of our survey participants but was also ranked as least preferred by four participants. This polarisation reflects the profile of survey participants and the large number of domestic non-bank lenders who tend to prefer residential development lending with residual stock being a natural extension/exit.”

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.